We have all heard about products that offer multiple features but still do not retain their market share. On the other hand, there are the “lucky ones” that seem to do nothing but get incredible demand. Why is this? What does it depend on, and how do we use it purposefully? It's all about understanding the dynamics of demand in your market and the ability to adapt your product to it, providing the necessary value for customers.

I think it is possible for ordinary people to choose to be extraordinary.

Elon Musk

Listen to the article in audio format:

Download the PDF Whitepaper of this artcle with all the graphs and illustrations that help you understand the described processes. Feel free to print it and share it with your colleagues.

We have all heard about products that offer multiple features but still do not retain their market share. On the other hand, there are the “lucky ones” that seem to do nothing but get incredible demand. Why is this? What does it depend on, and how do we use it purposefully?

I remember going on Craiglist 10 years ago and being surprised. How, in the late 2000s, can a service with such a primitive design be demanded by millions of people? I had a fresh iPhone3G in my hands, and the internet was full of beautiful and convenient services. I was wondering... didn’t they realize that in a few years all their users would go to more advanced and convenient competitors?

Yet, here I am today with an iPhoneX in my hands, and Craiglist is still popular, with very few advancements since its inception! How is this possible?

Using UXDA’s approach to analyze multiple similar cases, I seem to have found an answer to this question that could allow to better understand the development of products in general and financial services in particular. It should help identify the conditions under which some financial services are still in demand despite their outdated design and uncomfortable service, while others are on the verge of disappearing even while offering killer features.

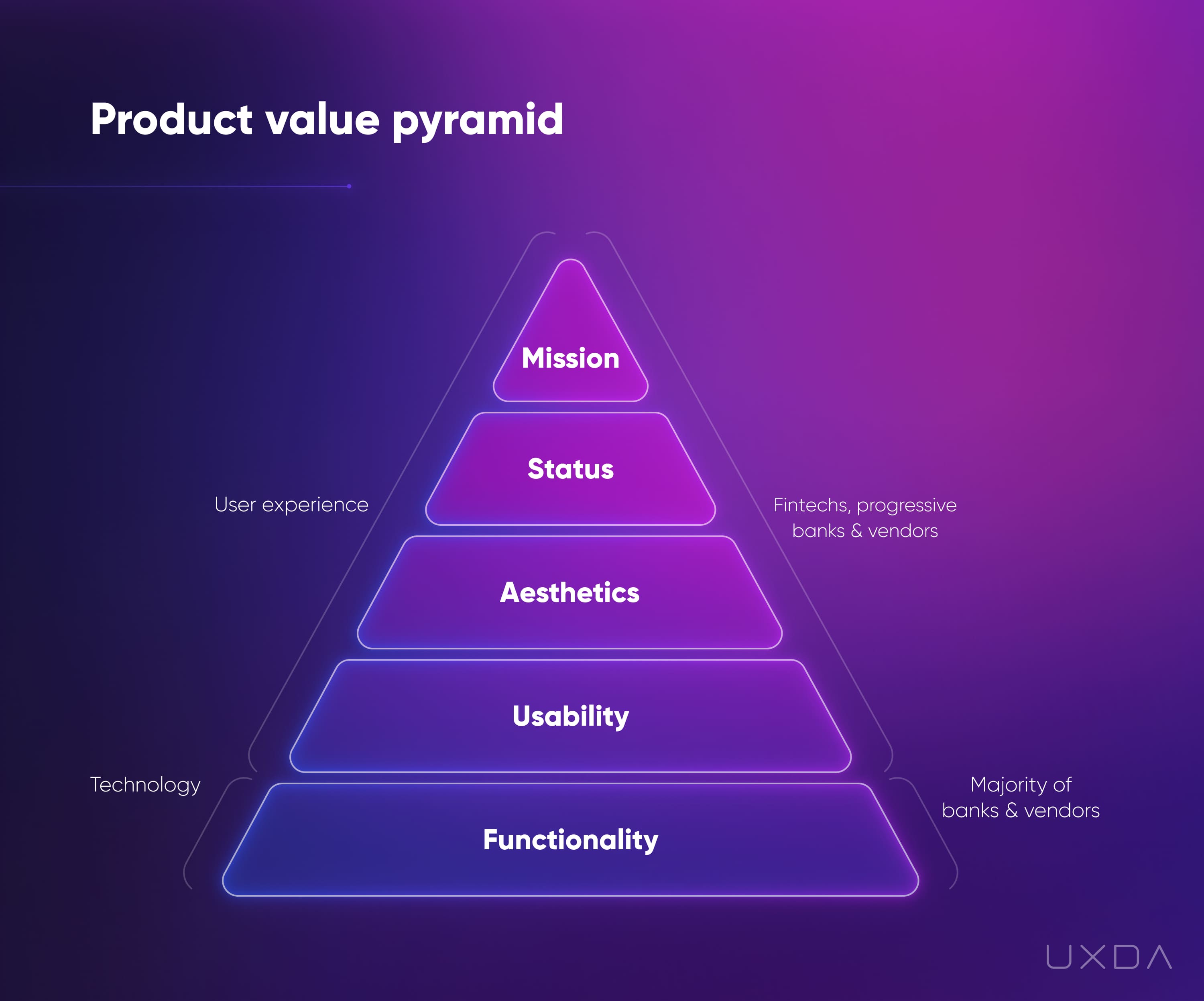

Financial UX Design Value Pyramid

I believe most people are familiar with the Maslow Pyramid. This hierarchy theory states that human needs and motives are developing stage by stage, and humans aren't interested in achieving the next level before completing the previous one.

The Maslow Pyramid

As for the market, I think you will agree that competition is the main force behind stimulating the development of the product value proposition. The greater the competition, the more the manufacturers are trying to meet the needs of people and gain a competitive advantage. This means we can draw a parallel with Maslow's pyramid and assume that, as competition grows, manufacturers will propel their products to higher and higher levels of human needs.

Thus, with each level of the pyramid, the value proposition of the product will become more and more humane. After all, in a highly competitive environment, products must increasingly match human nature to grow in popularity. At the same time, the market will become more and more fragmented, and the product niches will become narrower.

This is what we see in the banking market, in which new technologies have led to the emergence of many alternative services like Fintech. Incomers are often more convenient and better serve the specific needs of individual user groups.

So, if we take the pyramid of needs as a basis, we can extract levels of the Product Value Pyramid as follows:

1. Physiological Needs─Functional Value

Physiological Needs correspond to the Functional Value of the product. It's all about providing the desired result to the client by using the product features.

2. Need for Security─Usability Value

The Need for Security is associated with the comfort of the person, so here we can talk about Usability Value of the product. Ease of use satisfies the need for control and ultimately creates a sense of security and confidence in the product.

3. Love and belonging─Aesthetics Value

Love and a sense of belonging are emotions. A product can influence emotions through Aesthetics. Aesthetics allows us to enjoy things, service, relations and life in general. We are attracted to beautiful things; we value them and like to possess them.

4. Need for Respect─Status Value

The Need for Respect can be satisfied with the help of the clear Status Value of the product or, rather, its compliance with a certain lifestyle.

5. Need for Self-Actualization─Mission Value

The need for Self-actualization is the human desire to maximize the realization of his/her capabilities. Here, a product or service can inspire self-realization by offering to join an exciting large-scale Mission that brings value to the world.

The Maslow Pyramid and UXDA Product Value Pyramid

How It Works

Imagine that you have invented a product that provides a solution demanded by customers. All you would have to do is make it work properly and just enjoy your stable business and endless profit.

But, what if competitors copy the technology and start producing a similar product or service? Then you need to offer something unique that provides an advantage to your product and additional benefits to your customers. Simple functionality is no longer enough because everyone has it; you need to figure out additional value.

This is the moment when the competition takes an entrepreneur to the next level of the Product Value Pyramid. If functionality is not enough to compete, provide usability. If all the competitors have the same functionality and usability, add aesthetics. Or, if you need even more advantages, connect the product with the customer’s lifestyle by personalizing it; make it a symbol of his/her status. And, finally, you can go even further and state the mission to deliver ultimate value that will change the world.

As you can see, it is similar to the Maslow pyramid, but, instead of needs satisfaction, the main power to drive change is competition. If there's not enough competition and demand, the product would very likely be stuck in the functional stage. If you miss out on the market development stage and are stuck in one of the previous phases, the demand will most certainly decrease. For example, in a market in which most products are not just similar in functionality, but also quite convenient, customers don't need something more functional but unusable. Of course, price cuts can temporarily help until competitors offer more convenience for a similar price.

It should be kept in mind that the actualization of needs at the upper levels of the Maslow pyramid occurs only when the lower ones are satisfied. A person is unlikely to be concerned about the manifestation of love or the strengthening of his status if he is very hungry, or his safety is under threat. Also, a product offering top-level value in an unripe market may not find enough demand.

For example, if we go back in time when the main vehicle was a horse, most people couldn't even grasp the advantages of the invention of the first car, not to mention being able to appreciate cars that are more comfortable and beautiful. That's because it was completely irrelevant to them at that time. This clearly demonstrates that demand at the next value level of the market is formed as the demand in the previous level is satisfied.

Targeting the unique Product Value proposition at the top four levels (mission, status, aesthetics and usability) of the pyramid will help to maximize the needs of users through customer-centered product design. Therefore, when we ask what our user feels, how comfortable he/she is and whether the product solves their problem and fits their lifestyle, we are designing the user experience.

Level by Level

Let's find out exactly how the growth of demand and competition forms the uniqueness of the product at each stage of the Product Value Pyramid. We will test this model on one of the most developed industries─automotive.

You might ask: why cars if we work with finance? To hand over the model of the Product Value Pyramid as effectively as possible, I decided to look at it from a third-party industry. This way, it will be much more clear and easy to understand as this is your first encounter with this concept. After getting a taste of it, I will demonstrate how it applies to the banking industry.

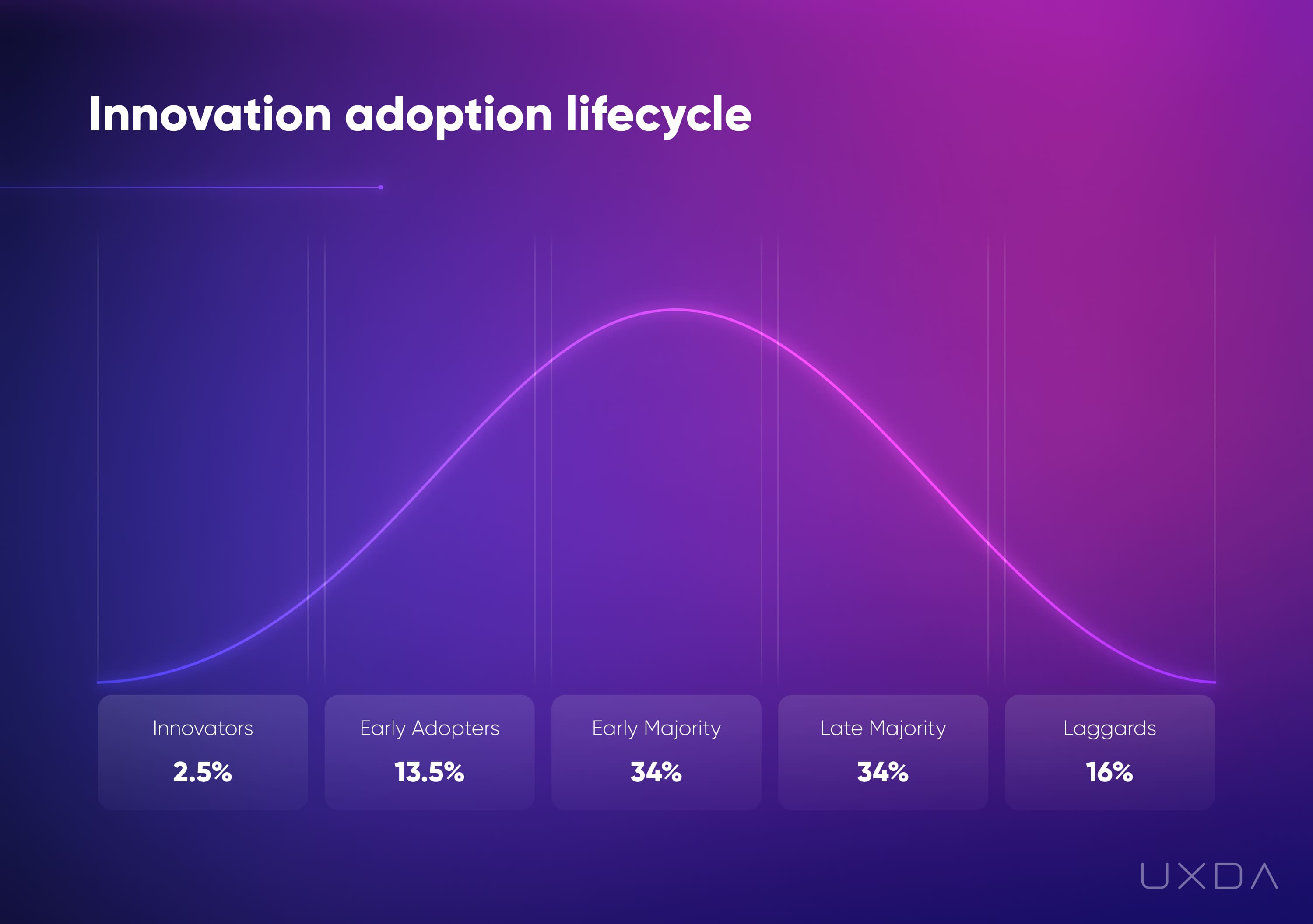

For an additional explanation of the model, I will use the innovation adoption lifecycle that clearly illustrates the dependence of demand on the adaptation of a new product in society.

1st Stage: Functionality

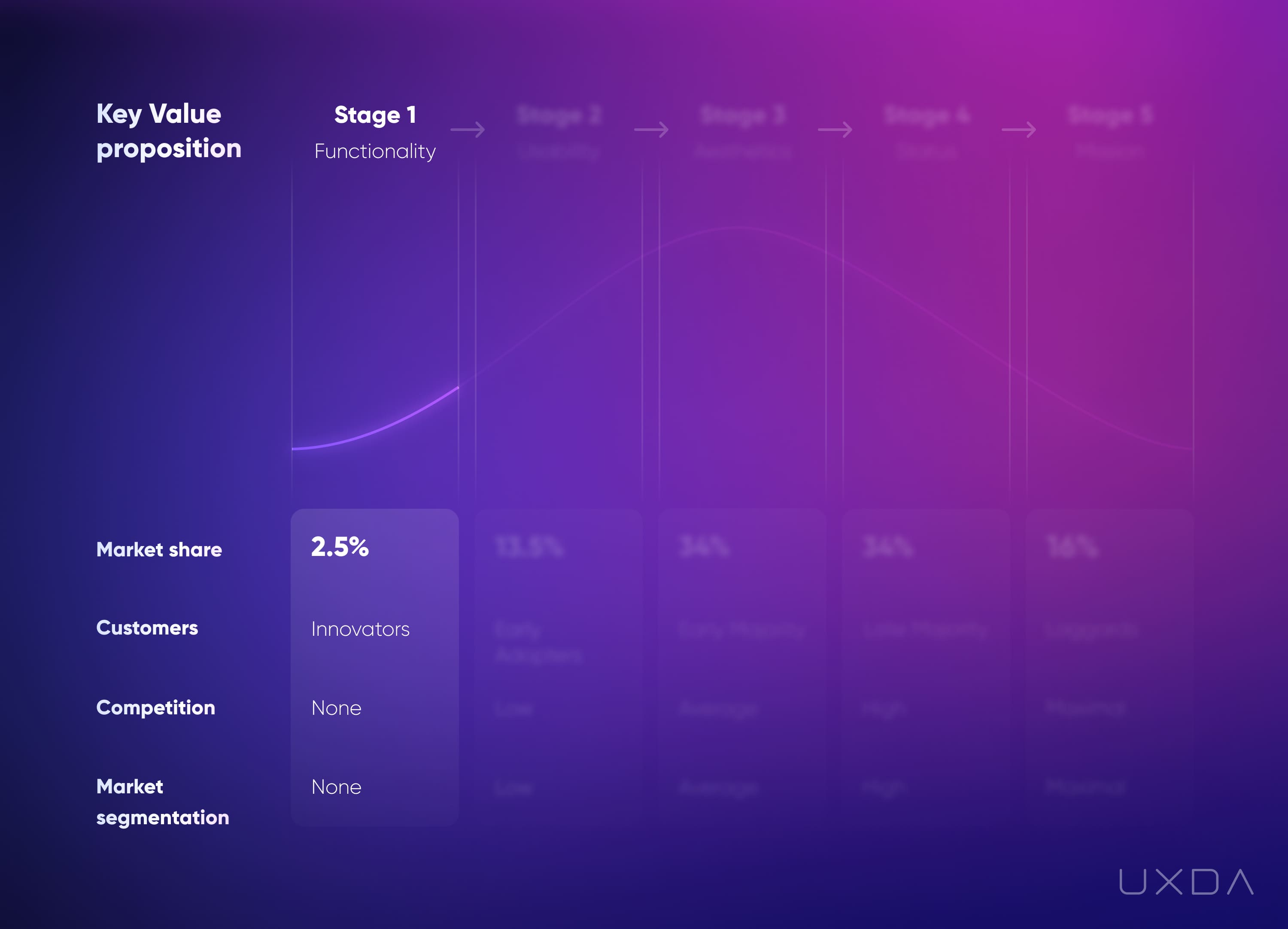

At the stage of market emergence, key decision-making criteria for buyers is determined by functionality. Functionality is used as the main unique feature of the product if it's among the first in the market. However, its disadvantages may outweigh the pros.

New technology may be inconvenient to use and may not be visually attractive. But, a certain category of buyers is ready to close their eyes to this and pay for the novelty. These are innovators, an average of 2.5% in any market, who want to be the first to try new solutions. At this stage, solutions that offer novelty through functionality typically enjoy the greatest demand.

An Example From the Auto Industry

The first buyers of cars were not familiar with the product, so they were interested only in its functional aspects: how to use it and how far and fast the auto could go compared to a horse. It was important to make the technology stable and raise the interest of the customers. So, the manufacturers weren't focusing on the convenience or aesthetics of their cars.

Therefore, the first cars didn't even have a roof and resembled a carriage without a horse. They were extremely inconvenient in driving control, and passengers even had to use special glasses and clothes. Nevertheless, for the buyer audience of innovators, this was enough, and they were eager to exchange the reliability of horses for the first unreliable machines.

What Does This Mean for Banking?

We can see similar processes in the financial industry. Despite several hundred years of history, the digital age has made the traditional players learn how to survive in the new digital service market. As a result, the financial industry is experiencing a total renewal and, at some point, began its ascent along the Product Value Pyramid from the bottom level.

The undermining of the industry by advanced digital technologies essentially translated banking services from the services category to the product category. Now, users aren't requesting a list of services at a bank branch but, rather, enter an online product or download a mobile application. This allowed banks to begin a wider expansion of their services using the internet to deliver their products beyond its local market, dramatically increasing the competition.

If we look at the development of digital banking, we see that most banks have already provided their customers with basic functionality. In particular, billions of users check their balance or transfer money using mobile banking. The technical level of digital banking solutions is very stable. Functional innovations at this stage become less common and do not provide a key competitive advantage demanded by users.

The active implementation of digital technologies has led to the disruption of the market monopoly of banks. Creating and launching a digital financial product has become relatively easy, and thousands of Fintech start-ups have poured into the industry. This started a transition to the next Product Value Pyramid stage with the emergence of convenient solutions, and not just functional, on the market.

Here, the banks using vendor solutions have a slight hitch. The speed of development of the B2B vendor solutions market is lower than the B2C mass banking market. The competition in the vendor market is quite low, since the development of a white label banking solution requires a large amount of time and resources. Therefore, most vendors are focused on providing banks with stable and secure high-quality functionality, especially when it comes to niche modules that basically have no competitors.

But functionality is not enough for the end users of banks, as the market for client solutions has moved to the next stage and has shaped higher expectations.

This analysis is confirmed by the fact that the active use of user experience design (UX) began five to seven years ago among FinTech startups. Banks, in turn, have only recently begun an active introduction of UX, customer experience (CX) and Design Thinking. As for the vendors, many of them still sell solutions that are difficult to use and are visually outdated, relying on its functionality as an advantage. Banks are forced to buy them despite the dissatisfaction of their users, since the vendors’ market does not offer alternatives. Therefore, some banks are forced to develop their own solutions or to customize the vendor's solution, increasing its convenience and attractiveness to their users.

Nevertheless, over the past few years, competition among vendors has begun to increase, and, in order to gain a place in the market, novices offer not just functional but convenient solutions. This becomes their real competitive advantage over traditional players. Time will tell whether traditional players will be able to upgrade their products to meet the market’s needs.

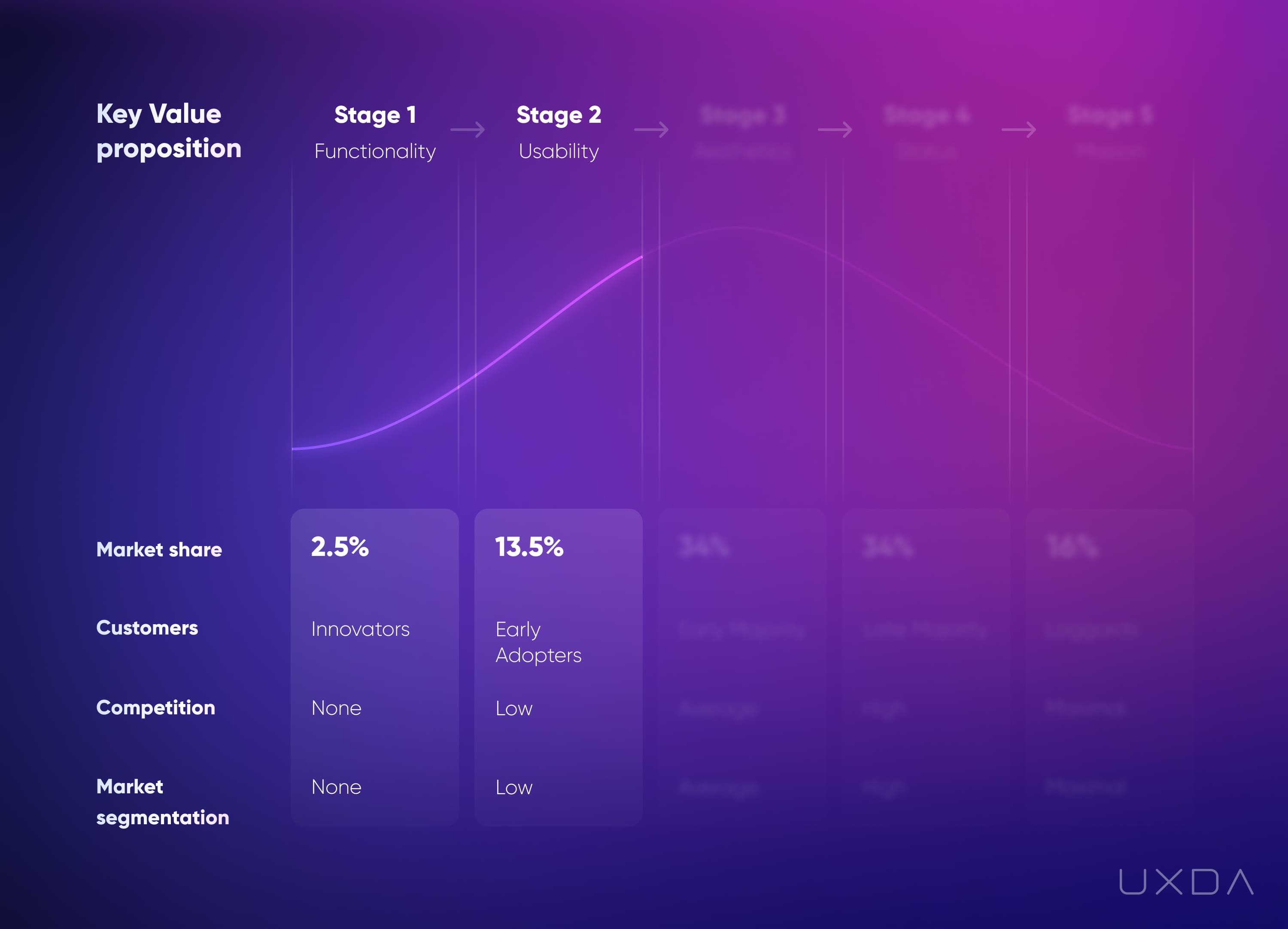

2nd Stage: Usability

When innovators tried out a new product and appreciated its advantages, they began to praise it, which stimulated the interest of early adopters, adding another 13.5% to the market. Demand began to grow, the production technology of a product or the provision of a service stabilized, and the market became interesting to competitors.

At this stage, functionality loses its key advantage. The technology is steadily reproduced, and more and more alternatives appear on the market. In the struggle for customers, manufacturers are beginning to think more and more about the convenience of their products or services. Expectations of customers are increasing, and they are no longer willing to put up with product issues.

An Example From the Auto Industry

So, the growth in demand leads to a new round of the competition. Competitors have focused on the convenience of cars. They began to offer cars that were easier to use, offering closed, soundproof cabs and wheel shock absorbers. This resulted in a significant increase in the demand for cars. And, manufacturers still didn't have to worry about aesthetics. As Henry Ford announced in 1909: “Any customer can have a car painted any color that he wants so long as it is black.”

What Does This Mean for Banking?

More convenient digital services have raised the financial user experience and user expectations to a new level. Consumers have felt that online and mobile banking should be convenient and pleasant to use. Thus, innovations in digital banking have moved from the Functionality stage to the Usability stage.

It is not enough to simply provide the ability to create an account online. It needs to be done faster, more easily and be more clear than its competitors. Instead of just providing the opportunity to transfer money using a mobile phone by filling out a long detailed form, they must offer the recipient the ability to quickly select a contact from the phone book and send money instantly.

I believe the perception of the majority of consumers of the banking market passed or is close to completing this stage. Because, for the majority of users, usability has become an indispensable element and not a special advantage of the digital product UI/UX design. It means we should look for the advantages that may surprise users at a higher stage of the Value pyramid.

Unfortunately, not all financial companies have revised their products and service development approach. Many of them are still confident that it is enough just to provide customers with the necessary functionality. And, they are sincerely surprised when customers switch to competitors complaining about a bad attitude, inconvenient service and overly complex UI/UX design.

3rd Stage: Aesthetics

Demand is growing along with competition, so more and more products with similar functionality and basic convenience enter the market. The product becomes interesting for the early majority, or the so-called pragmatists, who are convinced of its benefits and usability and will grow the market by another 34%.

Offering something special, something that can outcompete others, becomes really challenging. And, suddenly someone figures it all out: what if you offer users not just convenient function, but the opportunity to experience enjoyable emotions while using the product, and the market is introduced to not only functional and usable but also a more beautiful and appealing product?

Buyers gladly respond to this. They like that the product not only provides some benefits but also does it in a pleasant way, evoking positive emotions. So, aesthetics becomes the key competitive advantage of the product at this stage of the Product Value Pyramid.

An Example From the Auto Industry

The production of the world's first affordable automobile─the Ford Model T─ended in 1927. Overall, 15 million of these first cars were produced. The demand grew from 10,000 vehicles produced in 1909 to more than 2 million produced in 1923. Such fantastic demand inevitably led to the emergence of new competitors and the transition of the market to the next stage.

Aesthetics had become one of the most important characteristics of new cars. Consumers increasingly chose to enjoy the design of the car as well as comfort. Driving became enjoyable, delighting the driver with positive emotions. As a result, in the 1930s, more and more sophisticated and stunning cars appeared on the market.

Image source: wheelsage.org

What Does This Mean for Banking?

Despite the fact that some banking products have not yet reached the Usability stage, advanced FinTech services care a lot about not only the ease of use, but also the Aesthetics of their digital services UI (user interface). By the reaction of their customers, they see that visually attractive financial products evoke more positive emotions than a template design. Perhaps this can explain FinTech’s significant market success without incurring significant marketing costs comparing to banks.

Research confirms that consumers not only prefer more beautiful products, but also perceive their disadvantages more easily. Apparently, people are ready to be more forgiving of mistakes made not only by their beautiful friends, but also by beautiful services. However, we must bear in mind that the basic level of functionality and usability should not be compromised, as it’s addressed to the basic needs of users. Even the most beautiful car will fail if it doesn't move or is uncomfortable to drive.

The ongoing massive improvement in the functionality and convenience of digital financial products creates the conditions for using the Aesthetic value as a competitive advantage. And, we see that there are more and more beautiful financial products appearing on the market.

4th Stage: Status

Large growth leads to mass production. The cost of the product is reduced. The market is actively segmented by offering customers all new product variations depending on their capabilities, preferences and status. There are more and more conservative buyers on the market who are ready to pay more only if the product offers them some privileges.

The product is increasingly becoming an element of lifestyle, informing the public of certain status of its owner. At this point, manufacturers realize that they can produce products specifically for different customer audiences, creating a special set of characteristics in terms of functionality, convenience and aesthetics. These sets of characteristics are especially important to narrow target groups of consumers.

An Example From the Auto Industry

Automakers are beginning to actively segment the model range, trying to personalize the offer and conquer the market in parts. For the elite, they begin to produce luxurious and expensive cars, which, in turn, are divided into representative and sports; for families:- roomy and budget cars; for young people: flashy and compact; for workers: pick-ups, etc.

You can immediately determine to which social group a person belongs by their car. Social dimension is added to the functional and aesthetic characteristics of the product. The idea of a single functional product for all is transformed into many modifications for every taste and need.

Image source: wheelsage.org

What Does This Mean for Banking?

There are already quite a few financial products intended for a certain category of consumers. Status provides a powerful advantage as it personalizes experience for a specific audience. For example, “Step” - a mobile bank for teens, even before launch, collected approximately 500,000 customers on its waiting list. The company aims to address the needs of what it believes is an underserved market in mobile banking—the 75 million children and young adults under the age of 21 in the U.S., who are still being forced to use cash.

Nevertheless, given that the digital banking industry is at the Usability stage of the Product Value Pyramid, the Status value doesn't look so relevant for the majority of users. I’m not sure that a service that is not very convenient and visually appealing will interest me just because it is created specifically for people like me. After all, I just would not be pleased to use it.

Status value becomes an advantage only in the presence of appropriate Functionality, Usability and Aesthetics. This is the only way to achieve ultimate customer centricity. If these aspects are missing or do not match your users, then segmentation will not help. Consider the example of the digital-only bank, “Finn” by J.P.Morgan, which reached only 47,000 signups nationwide and decided to shut down.

As with cars, the segmentation of banking digital services can be incredibly wide. You can make an application for wealthy users, which will be available only if there is a certain amount in the account. It may offer special privileges and serve as a symbol of high social status. You can create a financial service for families that will be specialized in centralized family account management with a budgeting and control system.

Despite the fact that we see a lot of attempts to launch such services, the main peak of their popularity still seems to be ahead when market demand will be ready. Family cars, as well as the other specified categories of cars, also did not immediately reach mass demand.

5th stage: Mission

The product market is fully formed and has gone from growth to the stage of maturity. From the point of view of the S curve in market development, it is getting closer to a turning point. Demand continues to grow due to the late majority and skeptics.

And, suddenly a revolutionary offer appears on the market, which, at first, looks like another modification for a certain segment of consumers. However, it does not offer a new modification, but a new value reference point─a new world view beyond the usual benefits of the product.

Such a product is capable of undermining the existing market by offering an innovative vision that can transform this market, initiating a new technological revolution. Thus, the product ceases to be only a source of convenience or joy and becomes very significant for a certain group of consumers connecting with them at the level of values.

An Example From the Auto Industry

If we look at the automotive industry, over the past few decades, there is a feeling that competitors cannot come up with anything totally new. No significant changes have occurred for a long time.

But, recently, everything changed. In 2004, only a year after its foundation, an electric car startup, “Tesla Motors,” raised U.S. $7.5 million from Elon Musk in round A. As Musk stated in Recode’s interview: “Tesla is incredibly important for the future of sustainable transport and energy generation. The fundamental purpose, the fundamental good that Tesla provides is accelerating the advent of sustainable transport and energy production."

Image source: cars.com

Tesla had the courage to disrupt the automotive industry in spite of the oil lobby resistance. The value it brings to the world empowered millions of people and resulted in a high demand for Tesla automobiles. Musk wouldn't have experienced such success had he launched his product in a highly competitive market. What he did instead was disrupt the market. So, we see that, today, each car producer develops its own electric models.

Can the use of electricity transform the existing automotive market? Sure. First, it is a push toward digitalization and, accordingly, automatization of cars. The principles of driving cars will change dramatically, as will the conditions for their use. Probably the majority will stop seeing cars as a status indicator and will join sharing on demand.

Second, the use of batteries leads to a rethinking of transport and a possible modification in functionality, for example, cars in the form of drones or as delivery through underground tunnels. In any case, it is already clear that the automotive industry is already changing dramatically and will continue to evolve.

What Does This Mean for Banking?

The Mission stage or, one can say, the ideological stage of the Product Value Pyramid, is still far from the banking market. Finance has only recently begun to pay attention to humans and face their needs, pain and fears. And, the majority of consumers are not yet ready to go after the ideological financial product.

It may seem that Bitcoin has taken over the mission to change the financial world. But, if you take a closer look, this product just became a solution for anonymizing cashless transfers, as well as an investment tool. The blockchain contains a much greater potential for changing the world.

However, blockchain is not a product with a mission; it is a technology that can disrupt the financial and related industries. Today, it looks like an electric motor and a battery without Tesla. But, as we know, the first electric cars appeared a hundred years ago but only recently began to enter the mainstream. And, the influence of Tesla is difficult to overestimate.

Perhaps soon, we will see a hero product based on blockchain or other technology that has a mission to change the financial industry, and millions who are ready to change the world will follow it. But, for this, any technology must first become functionally stable, usable and beautiful and adapt to the needs of various consumer clusters.

Monopoly is the Exception in the Model

The Product Value Pyramid model also explains well why some businesses that do not pay special attention to the upper stages, i.e. Usability, Aesthetics, Status and Mission, still maintain their position in the market, as well as a high level of demand.

It's all about monopoly. If, due to any reason, the market entry barrier is too high and competition cannot be formed, then users are forced to accept functionality without convenience and beauty.

Let's get back to the example we covered in the first part of this article. Craiglist has not changed much since 2000. Many people wonder how this is possible in the age of rapid growth in digital technologies, the internet and user services. This is easily explained in our model.

Craiglist was one of the first to offer users a platform for online classified ads for used items. Their functionality was enough to attract innovators and early followers. When the competitors realized the viability of this market, they launched their platforms with a more convenient interface. But, the uniqueness of the niche was that buyers go where there are more offers, and sellers go where there are more buyers. Audience became part of the functionality, that's how Craiglist nailed it.

Thus, competitors could not provide functionality at the same level because the Craiglist community had become its functional advantage unavailable for copying by competitors. This allowed Craiglist to essentially monopolize the market and preserve it in the functional stage without straining about its own convenience or beauty.

Similar services can be found everywhere, including in the financial industry. It's about niche products that have virtually no competition. This allows them to remain unchanged, completely ignoring the expectations of users and their need for more enjoyable solutions.

However, in the more competitive domains, the lack of user care leads to a redistribution of demand flows in favor of more progressive competitors using powerful design tools and Design Thinking approach to provide best possible CX and UX to their customers.

Conclusion

The Product Value Pyramid allows us to understand why, in the Digital Age, user-oriented design is becoming not just popular, but also taking on an increasingly important strategic role. UX design in banking industry is becoming a key element to ensure compliance with the market stage of a Product value to gain significant competitive advantages.

By only focusing on the convenience, aesthetics and status of the banking product, you can engage digital users. But, this is not enough to create an attractive-looking interface, it is necessary to integrate user centricity into all levels and processes of the company, putting the delightful user experience at the forefront. We will discuss how to achieve this in the next article about our second model─ UXDA Pyramid of Financial Design Integration.

Get UXDA Research-Based White Paper "How to Win the Hearts of Digital Customers":

If you want to create next-gen financial products to receive an exceptional competitive advantage in the digital age, contact us! With the power of financial UX design, we can help you turn your business into a beloved financial brand with a strong emotional connection with your clients, resulting in success, demand, and long-term customer loyalty.

If you want to create next-gen financial products to receive an exceptional competitive advantage in the digital age, contact us! With the power of financial UX design, we can help you turn your business into a beloved financial brand with a strong emotional connection with your clients, resulting in success, demand, and long-term customer loyalty.

- E-mail us at info@theuxda.com

- Chat with us in Whatsapp

- Send a direct message to UXDA's CEO Alex Kreger on Linkedin